Shorts Profitable in Private Credit Stocks

Author:

Ihor Dusaniwsky, Head of Predictive Analytics

Mixed Short Selling & Covering in the Sector

The collapse of auto parts supplier First Brand Group and subprime auto lender Tricolor Holdings has spurred a reaction to the increased credit risk of Business Development Companies (BDCs) which provide equity financing, customized debt, and debt capital to smaller companies. JPM’s Jamie Dimon warned that more credit issues may arise in the market “when you see one cockroach, there are probably more.”

Total short interest in the sector is $1.22 billion with the sector not Crowded on the short side and not Squeezable due to recent short-side profits. There are $12.31 billion of Passive long shareholders and $4.54 billion of Active Long shareholders in the sector.

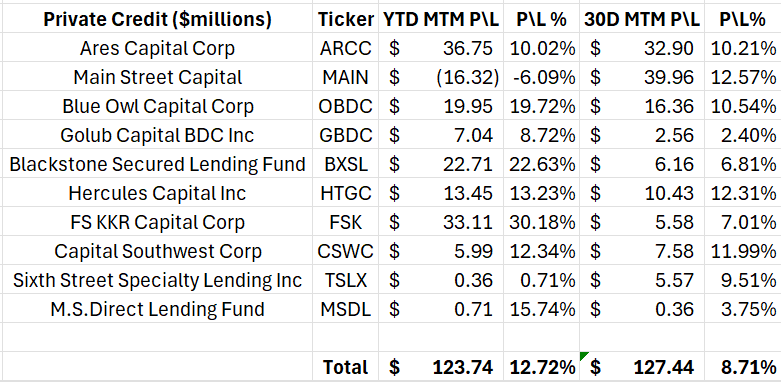

Shorts have made all of their year-to-date profit over the last thirty days.

MAIN is the only “battleground stock” in the sector with an equal amount of active long and short holdings.

We have seen mixed short selling and short covering in the sector. For the year, short sellers have been active with a net $191 million increase in short selling with GBDC & CSWC having the most short selling while ARCC & HTGC had the most short covering. Over the last thirty days, we have seen net short covering of $6.2 million with OBDC & GBDC the most shorted and ARCC & MAIN seeing the most short covering.

Private Credit short sellers have been profitable in 2025 with $123.7 million in year-to-date mark-to-market profits, +12.72% for the year. But all these profits were earned over the last thirty days with short sellers up $127.4 million, +8.71% over the last thirty-days.

On the long side we see $12.3 billion of Passive long holdings (mutual funds, pension funds, ETF providers, etc.) and $4.5 billion of Active long holdings (hedge funds). The most widely held stock by hedge funds is ARCC with 909 hedge fund accounts holding long shares and FSK & OBDC a distant second and third.

None of the stocks in this sector are Crowded on the long side with only three stocks topping a 60 score (a 50 score is neutral, and a 80-100 score is considered to be crowded).

The only Private Credit stock that is considered a “battleground stock” is MAIN, having a 1.03 Active Long Holdings vs Short Interest ratio. With an equal amount of active long and active short shareholdings we should see increased volatility in this name.

There has been selective short selling and short covering in these stocks with those names with stronger balance sheets and less risky exposure seeing short covering and those with riskier exposure seeing short selling.

Expect more volatility in this sector if more credit and default issues become known. But if interest rates continue to decline, credit risk decreases, we may see short covering as short sellers look to realize their recent mark-to-market profit windfall and help drive stock prices higher.

Want to know more? Access this data in real time using S3’s BLACK APP & BLACK MAP

The information herein (some of which has been obtained from third party sources without verification) is believed by S3 Partners, LLC (“S3 Partners”) to be reliable and accurate. Neither S3 Partners nor any of its affiliates makes any representation as to the accuracy or completeness of the information herein or accepts liability arising from its use. Prior to making any decisions based on the information herein, you should determine, without reliance upon S3 Partners, the economic risks, and merits, as well as the legal, tax, accounting, and investment consequences, of such decisions.